The one-stop shop (OSS) and distance selling from July 1st, 2021 are the biggest reform of the sales tax for EU online trade and should finally simplify intra-Community trade. Taxation takes place from a total value of €10,000 in the country of destination, the previous delivery thresholds no longer apply. VAT only has to be registered with one central registration office per country, making VAT registrations in individual countries superfluous. German online retailers who ship their goods from warehouses in Germany to private customers in other European countries must subject their sales to foreign sales tax regardless of whether a delivery threshold is exceeded. In this article, online retailers will find an overview of important changes.

So far, the so-called “recipient principle” has applied to deliveries from an entrepreneur to an end consumer (B2C deliveries) within the EU. This means that the delivery is taxed at the recipient’s registered office. In order not to be immediately subject to VAT registration in every EU country, delivery thresholds were specified by the respective countries. In Germany, this value is currently €100,000. If this limit is not exceeded, a cross-border delivery may be taxed at the home tax office.

If the delivery threshold is exceeded, this restricts small dealers in particular, since the registration process in the individual countries takes a lot of time and a local tax consultant usually has to be consulted.

In order to simplify the time-consuming procedure, the EU has introduced a new regulation for the treatment of sales tax in the case of cross-border e-commerce.

We have therefore summarized below what online retailers will have to consider from July 1st, 2021.

1. What is a one-stop shop?

Loosely translated, the one-stop shop is referred to as the “single point of contact”. The one-stop shop makes it possible to document all previously required bureaucratic steps that lead to the achievement of goals in one place.

The communication processes are to be shortened and administrative tasks optimized.

The resulting simplifications offer significant advantages, especially for smaller online retailers, and can lead to a reduction in costs.

2. How has tax liability been treated so far?

Ever since the European single market was established in 1993, the tax liability for mail-order sales from entrepreneurs within the EU to an end consumer in the country of the recipient has been there.

If the delivery threshold specified in the respective country is exceeded, the following steps must be observed:

3. How is the tax liability treated by the introduction of the OSS procedure?

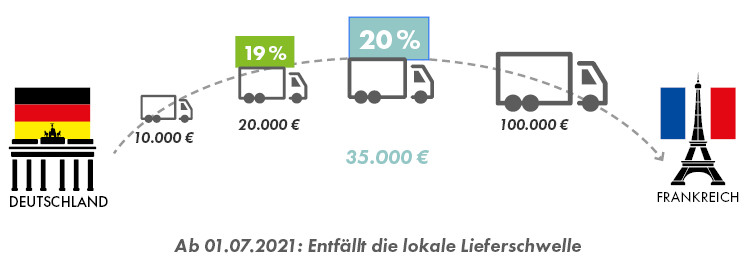

The national delivery thresholds of the EU countries are to be dropped. The EU-wide delivery threshold of €10,000 net takes its place. Deliveries from entrepreneurs to end consumers in other EU countries will be taxed in the country of destination from July 1st, 2021 as soon as the threshold of €10,000 is exceeded.

It should be noted here that the previous delivery thresholds set individually for each Member State will no longer apply and will be replaced by a single so-called “pan-European” threshold – for all Member States together.

Example:

Entrepreneur DE supplies customers without UID in

• Austria for €7,000

• France for €2,000

• Czech Republic for €2,100

Solution:

The threshold of €10,000 has been exceeded. The place of delivery is in the respective Member State. There the sales tax arises with the tax rates applicable there. Entrepreneur DE can declare its sales in OSS procedures.

4. Changes for companies using the one-stop-shop procedure

With the new regulation, the EU is pursuing a simplification and more transparent processes, which should promote the Europe-wide harmonization of sales tax law.

In the future, according to § 18j UStG, EU companies that provide taxable services to non-entrepreneurs will have to report these sales in their country of residence.

As a result of the new regulation, the delivery thresholds for goods movements that previously applied in the respective country will no longer apply and instead a uniform delivery threshold of €10,000 will be set for all EU countries as a whole. As part of the standardization of delivery points, there will be a central office where sales tax returns will be submitted.

The introduction of the one-stop-shop procedure creates the organizational structure and the technical requirements for a simplified report. Specifically, the affected sales are registered via the Federal Central Tax Office (BZSt).

A VAT registration in other EU countries is therefore no longer necessary for online retailers in all countries in which they operate, and a separate registration and payment of VAT is no longer necessary.

5. Who is interested in the one-stop-shop procedure?

Before registering with the BZSt, online traders should check carefully whether the participation criteria for the OSS procedure have been met.

According to the BZSt list, the procedure is aimed at the following target groups:

Entrepreneurs who are based in Germany and:

In addition, the OSS procedure is aimed at entrepreneurs who are not based in the EU and have a domestic facility such as a warehouse from which goods are delivered to private individuals in other EU member states.

6. When do the new regulations apply?

Officially, the regulations for the one-stop-shop procedure apply from July 1st, 2021 for all deliveries of goods within the EU and the resulting sales tax.

It remains to be seen whether the technical implementation and the integration of a suitable IT interface for reporting will be completed by all online retailers by this time.

Online retailers who are already registered for the Mini One Stop Shop (MOSS) process automatically take part in the OSS process.

7. What can online retailers do now?

Registration with the BZSt has been possible since April 1st, 2021 and should be done by all online retailers who deliver to end customers in other EU countries and want to participate in the OSS procedure.

8. When are the reports to be made via the OSS?

Current note: since registration for the OSS can only be made before the start of each quarter, the decision to participate in the first possible taxation period of the third quarter of 2021 must be made by June 30th, 2021.

Not sure if you meet the registration requirements or have questions about what’s new with the e-commerce package?

Feel free to contact us using the form and we will find a suitable consultation appointment – whether online or in person!

You are currently viewing a placeholder content from Vimeo. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More Information